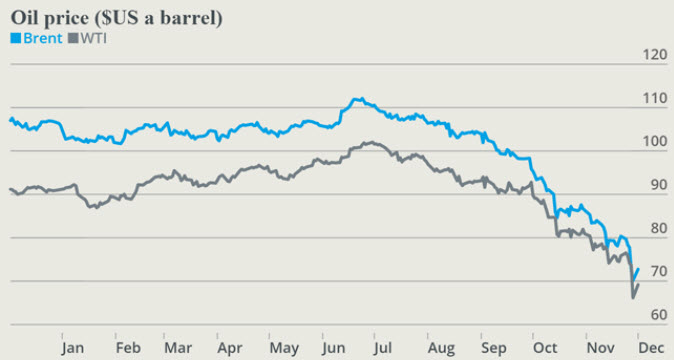

EDMONTON, Alberta – The price of oil in recent months has now struck a crippling blow to insurance companies across Canada. Hundreds of oil and gas operators have recently filed claims on their losses as prices drop in to the $45 per barrel range, expecting massive payouts from insurance companies.

The insurance policies that the companies took out were largely seen as non-viable when they were purchased. Be it ego or naivety, the insurance companies did not think the price of oil would fall to below $50 a barrel within the terms of the policies. Now, they are rethinking that poor decision.

The insurance companies were aiming to expand their market portfolios into oil and gas diversity in a plan to cash in on the oil boom in Alberta. The ever growing market for liability insurance on energy commodities was alluring, and the idea of another oil crash being almost unbelievable.

An oil price scenario that actuarial scientists with insurance companies did not anticipate.

This dangerous combination of factors has now left many larger insurance companies scrambling to find the cash to payout claims against the losses oil companies are seeing in recent months. Beyond that, many of the major insurers are finding it hard to see a profit in the next few years without creative ways to recoup their money.

As the floods from 2013 in Alberta took a large financial toll on all insurance companies, well into the billions, they are now going to have to dig into the this year’s company bonuses to help with covering this potential 2015 catastrophic oil loss. Many companies may fall short of getting a any bonuses at all. There are also rumours of special catastrophe teams being reassembled to help mitigate this potential fall of commercial insurance claims through the oil companies.

Henry Fuddeduk, Inpact Insurance COO

We wrote the policies under capital devaluing procedures to find the lowest threshold within a net present valuation, using the economic 3P scoring analysts gave us. We hedged our policies along the $50 price boundary and never expected to pay out. We thought the oil companies were just buying them for optics. We were wrong.

Our problem is that we wrote policies insuring losses from $80 and lower once the price hit $50. We are now seeing claims for $30 or more per barrel each of our insured is producing. – Henry Fuddeduk, Inpact Insurance COO

The policies were basically bought for the same purpose of crop insurance. If oil tanked, these companies could get paid out for losses and stay afloat. Obviously the insurance companies never saw it coming, and not they stand to lose hundred of millions of dollars if not billions in payouts. It will break some, but others will simply hike rates in other sectors to cover the losses.

Sandy Watchoowach, PR Manager at Wawasucka Canada Fidelity

If we pay these out, and I say if, we will have to make up the shortfall in other areas. Alberta will face 20-30% rate hikes on property insurance, we will require security deposits on vehicular collision insurance for at least 40% of the value of the vehicle, plus a rate hike of 15% across the board for auto premiums. We can handle it, but it will take some finesse. – Sandy Watchoowach, Wawasucka Canada Fidelity

So far 2P News has learned that PNRL, Mooncor, Best West, Finite Reseources, and Gheytex Energy have all filed for the Petroleum Failure Insurance. Several other large operators have been reported to follow suit in the following weeks.

With a recorded 432 PFI policies purchased over the last several years, it can be expected the numbers will rise through the end of Q1 and well into Q2.

It does however remain to be seen if the Insurance Board of Canada will need to step in to stall settlements due to the unusually high nature of said settlements in an effort to save its own ass.

{kind=link}